What Are xETFs Daily Income ETFs?

Rethinking How Income Is Generated from Equities

Income strategies in equities often rely on selling options to generate cash flow, with covered calls as one widely used approach. However, that approach can involve a tradeoff. Selling call options can limit participation if markets move higher.

xETFs’ Daily Income ETFs are designed differently. Instead of applying options across an entire portfolio, they use options more selectively, with the intent of generating option premium while keeping a larger portion of the underlying stock exposure.

The goal isn’t to maximize yield at all costs, but to seek income while remaining exposed to the underlying stock.

What the Strategy Does

The strategy is designed to maintain exposure to a single stock (for example, NVIDIA or Tesla) while writing call options on just a portion of that exposure. The strategy may sell call options on up to 25% of the equity position but will initially target selling only 10%.

The options used are short-dated (meaning they typically have near-term expiration dates ranging from zero to five days) and will be reset daily. The approach is intended to collect option premium more frequently than longer-dated option structures. The option position is closed by the end of the trading day, leaving the underlying stock exposure fully uncapped overnight.

This structure is designed to keep most of the exposure to the underlying stock, while seeking to generate option premium.

Why “Daily” Matters

Designed for Upside Participation

A simple idea behind frequent option-writing approaches is that selling options more frequently can change the tradeoff between premium collected and how much of the portfolio is overwritten.

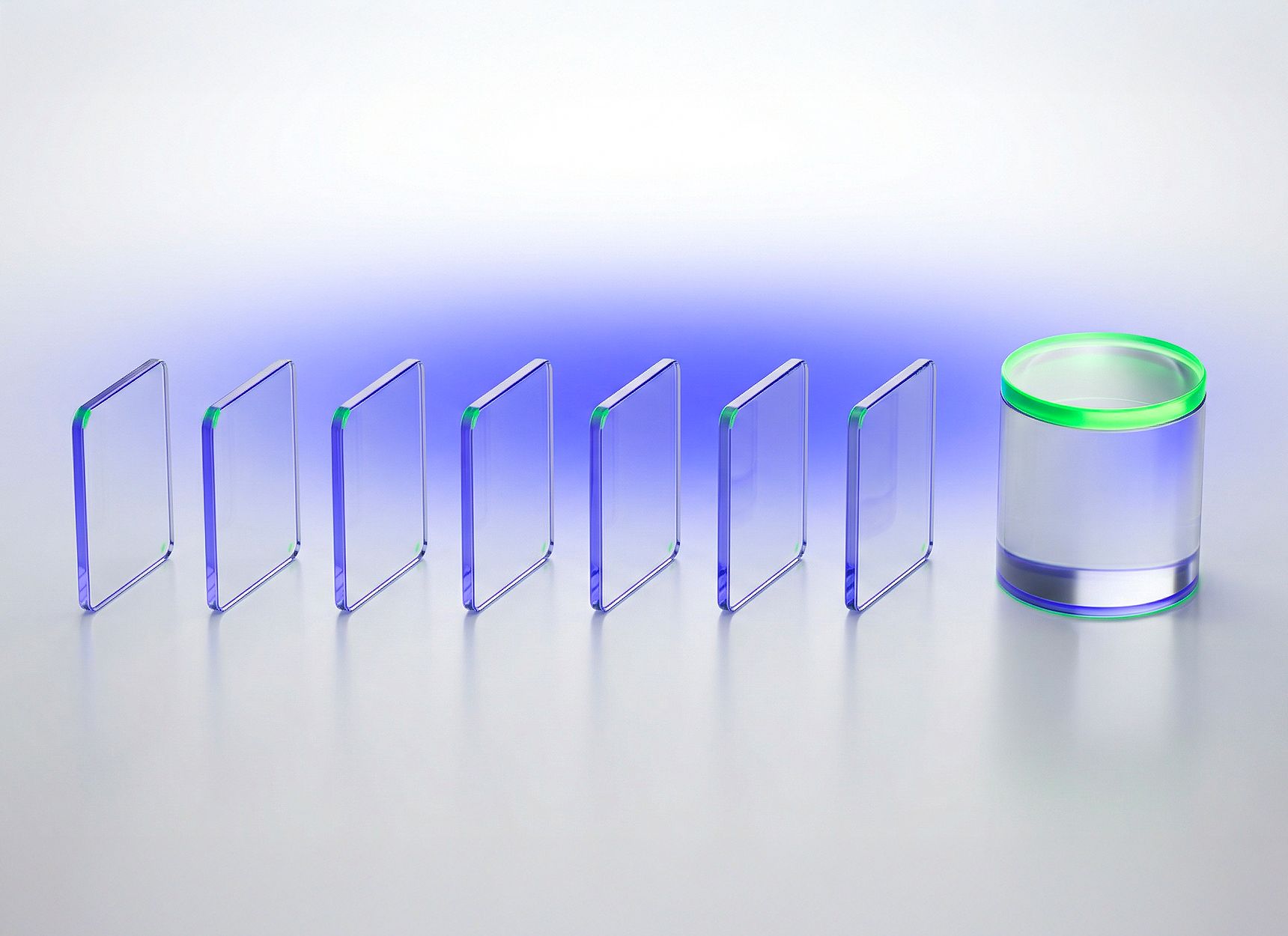

Shorter-dated options allow income to be generated in smaller, more frequent increments, often adding up to more than longer-dated options. For example, a one-year option may generate approximately 9% in premium [1], while a one-month option may generate around 2.4%. Selling the one-year option once produces that 9%, whereas selling the one-month option 12 times over the year would generate closer to 30%.

Because option premiums are generated more frequently, less of the portfolio needs to be overwritten. In this example, only about one-third of the portfolio would need to be overwritten to match the same 9% of premiums.

We apply this same principle on a daily basis. Because options are written daily, the strategy can generate income while only overwriting a small portion of the portfolio (up to 25% with an initial target of 10%) leaving the majority uncapped and exposed to upside.

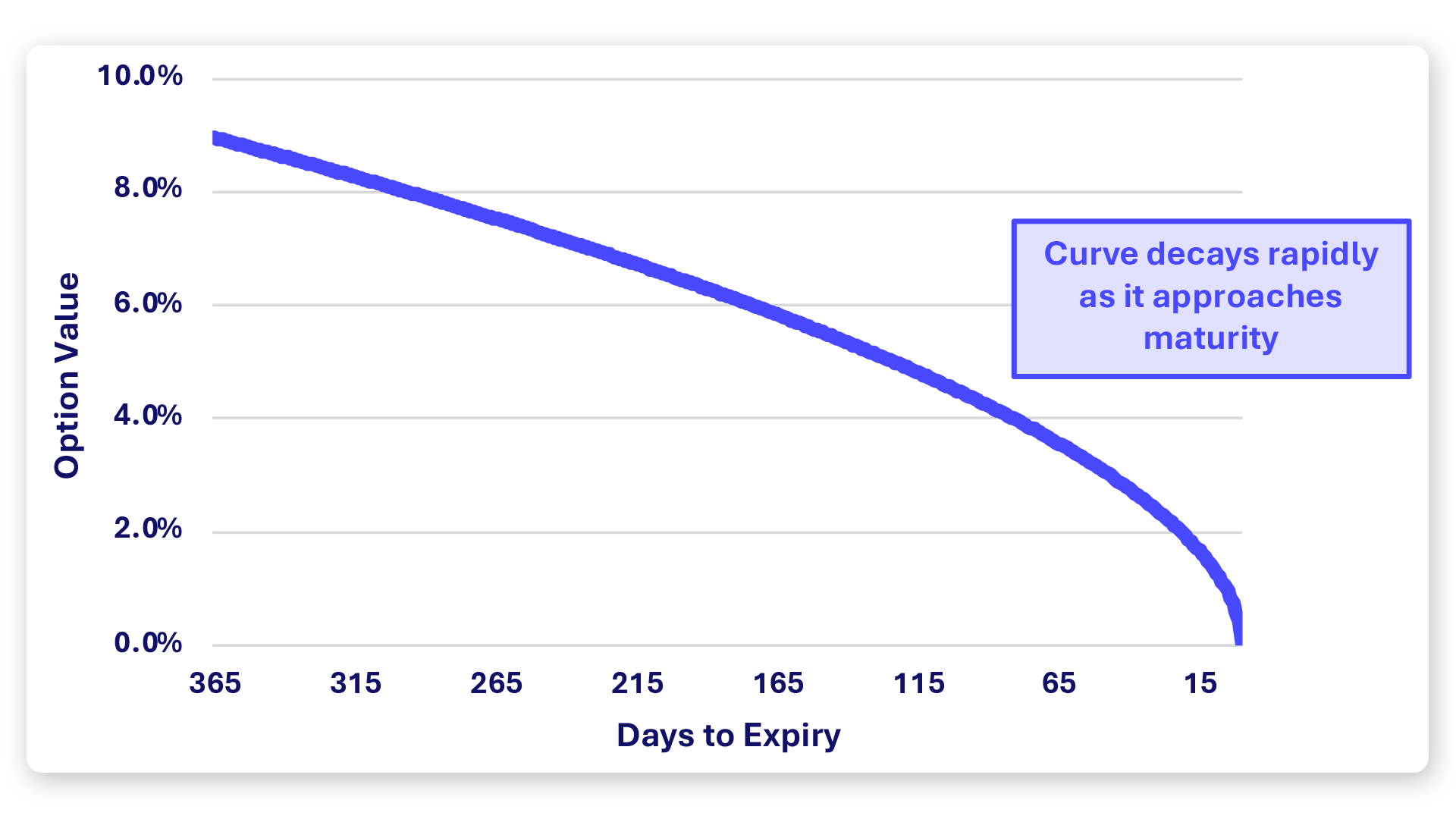

More Efficient Time Decay Capture

Option values do not change linearly with time. In many options models, time value is often described as scaling non-linearly with time to expiration (commonly approximated by the square root of time, all else equal). Selling options close to expiration may thus generate more premium and repeatedly capture this faster decay than if the relationship were linear.

Option Time Value only. Not representative of the total value of an option, which is affected by other factors.

By focusing on shorter-dated options and resetting positions daily, the strategy seeks to capture time decay more continuously than approaches that rely primarily on longer-dated options.

Seeks Full Overnight Equity Exposure

Since option positions are closed by the end of the trading day, investors remain fully exposed to overnight price movements, which can be meaningful and can occur for many reasons, including earnings announcements, macro developments, and geopolitical events.

A meaningful portion of equity returns has historically occurred outside of regular trading hours. Some research even shows that, over long periods, the majority of market gains have been realized overnight rather than during the trading day.[2]

Taken together, these three elements reinforce the core idea: seek to generate option premium more frequently, without surrendering most of the underlying exposure.

Learn more about xETFs Daily Income ETFs.

View NYYY ETF >

View TYYY ETF >

How the Strategy Works

The fund is designed to follow a systematic approach:

- The portfolio is designed to maintain exposure to the underlying stock

- Each trading day, it will sell short-dated call options on a limited portion of notional (target 10%)

- On the portion not overwritten, the full stock exposure is retained

- The call option position is repurchased by the end of the day

- 100% exposure to stock performance is kept overnight and over the weekend

The fund intends to make distributions weekly, which may be sourced from income, capital gains, and/or return of capital.

A Different Approach to Standard Income Strategies

There are common approaches to generating option premium from equities.

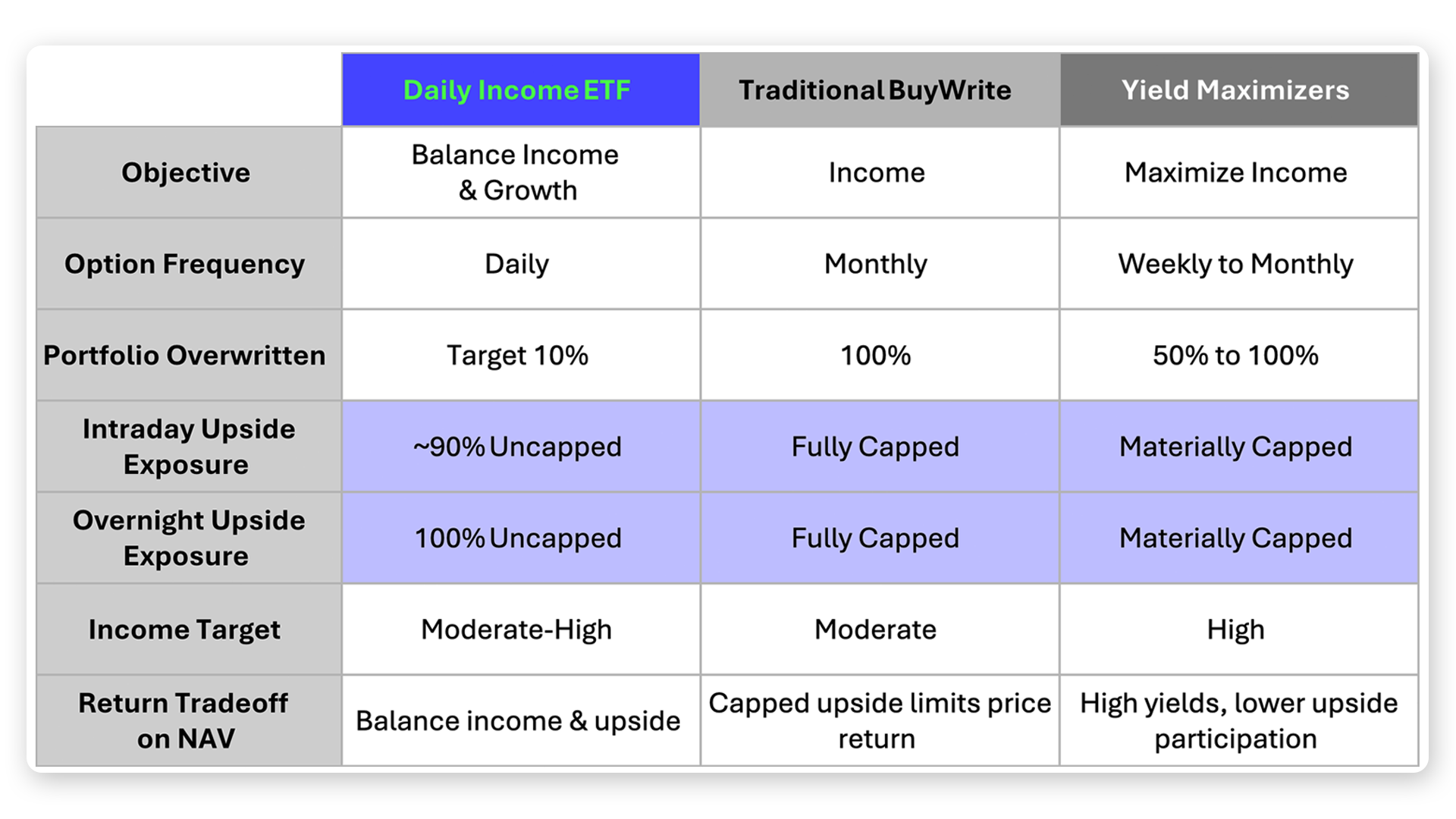

Traditional buy-write strategies sell call options across a larger portion (or all) of a portfolio, which can meaningfully limit upside participation if the underlying rises. Other approaches may increase overwrite levels, adjust strikes, or change option frequency in ways that can increase premium collection, while also increasing the likelihood of foregone upside and/or different risk exposures.

Daily Income ETFs are designed differently.

By using options on a smaller portion of the portfolio and resetting more frequently, the strategy is intended to keep significant exposure to stock performance, while still earning option premiums.

Here’s a high-level comparison of typical structural characteristics (actual fund implementation may differ):

- Option frequency: Daily option writing vs. monthly/weekly in other approaches

- Portion overwritten: Limited overwrite — Daily Income ETFs will target overwriting 10% — vs. higher overwrite levels

- Upside exposure: A larger portion of the portfolio is designed to be retained in Daily Income ETFs vs. other approaches

Potential Use Cases for the Strategy

Daily Income ETFs can be applied in a range of contexts, depending on the objective:

Whether enhancing income, complementing bonds, or replacing covered call strategies, Daily Income ETFs can complement a range of investment strategies.

Putting It All Together

Daily Income ETFs represent a different way to seek income from equities.

By using shorter-dated options more frequently and on only a portion of the portfolio, the strategy is designed to collect option premium in smaller, repeated steps without overwriting the entire position.

Traditional approaches often generate option premium by overwriting more of the portfolio, surrendering a lot of upside. Daily Income ETFs are designed to seek option premium while remaining significantly exposed to the underlying stock.

[1] Using Black-Scholes options pricing model for an at-the-money call option, with 20% volatility, 3.5% interest rate, and 1.2% dividend yield

[2] Glasserman, Paul and Krstovski, Kriste and Laliberte, Paul-Robert and Mamaysky, Harry, Does Overnight News Explain Overnight Returns? (July 02, 2025). Columbia Business School Research Paper No. 5336382.

Carefully consider the Funds’ investment objectives, risk factors, charges and expenses before investing. This and additional information can be found in the Funds’ Prospectus and Summary Prospectus, which may be obtained by visiting www.xETFs.com/investor-materials. Read the Prospectus and Summary Prospectus carefully before investing.

Exchange Traded Concepts, LLC serves as the investment adviser. WallStreetX ETFs, Inc. dba xETFs serves as the sub-adviser. The Funds are distributed by Foreside Fund Services, LLC., which is not affiliated with xETFs, Exchange Traded Concepts, LLC, or any of its affiliates.

Investing involves risk, including possible loss of principal. The Fund’s return may not match or achieve a high degree of correlation with the return of the Index. To the extent the Fund’s investments are concentrated in or have significant exposure to a particular issuer, industry or group of industries, or asset class, the Fund may be more vulnerable to adverse events affecting such issuer, industry or group of industries, or asset class than if the Fund’s investments were more broadly diversified. Issuer-specific events, including changes in the financial condition of an issuer, can have a negative impact on the value of the Fund.

A new or smaller fund is subject to the risk that its performance may not represent how the fund is expected to or may perform in the long term. In addition, new funds have limited operating histories for investors to evaluate and new and smaller funds may not attract sufficient assets to achieve investment and trading efficiencies.

Shares are bought and sold at market price (closing price) not net asset value (NAV) and are not individually redeemed from the Fund. Market price returns are based on the midpoint of the bid/ask spread at 4:00pm Eastern Time (when NAV is normally determined) and do not represent the return you would receive if you traded at other times. Brokerage commissions will reduce returns.