What Is Implied Volatility and Why It Matters

What Is Implied Volatility and Why It Matters

Two call options with similar structures and maturities can pay out very differently. The gap almost always comes down to implied volatility, one of the most important and most misunderstood concepts in options pricing.

What Volatility Measures

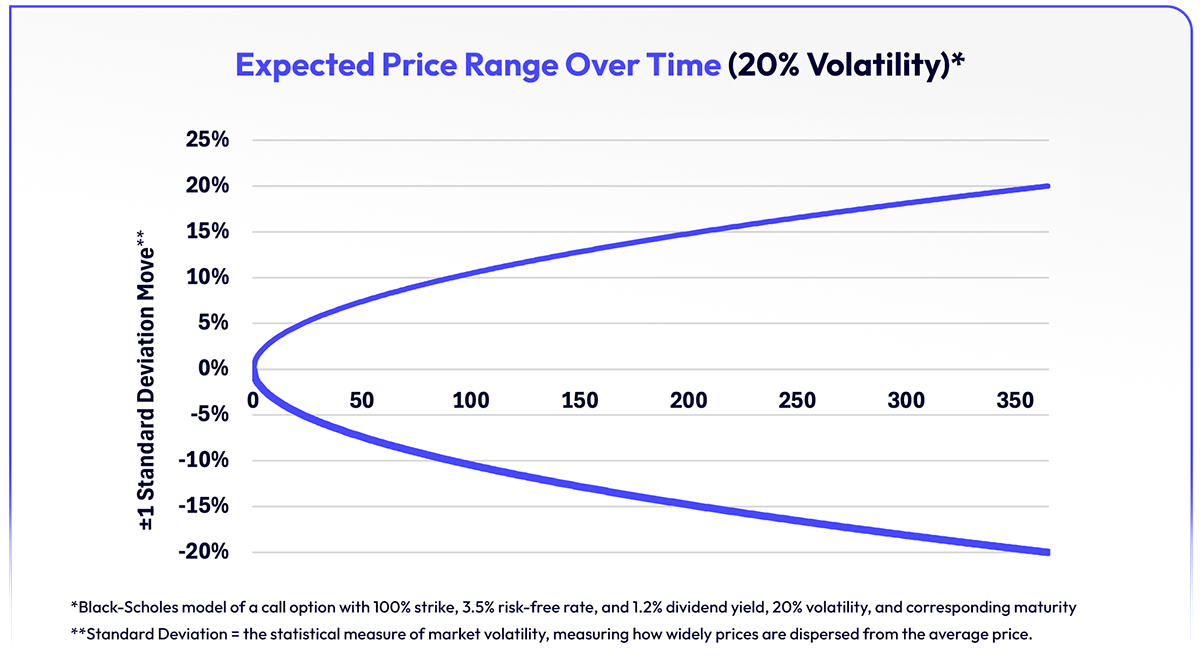

Volatility measures how much a stock tends to move, not in any particular direction, but in terms of the size of the swings. A stock with 20% annualized volatility is expected, with roughly 67% confidence, to finish within 20% of today's price over the next year. At 95% confidence, that range widens to about 40% in either direction, assuming a normal distribution of investment returns. A higher volatility number means a wider range of possible outcomes. Time compounds this: the longer the holding period, the wider the range, even for a relatively calm stock.

How Volatility Drives Option Prices

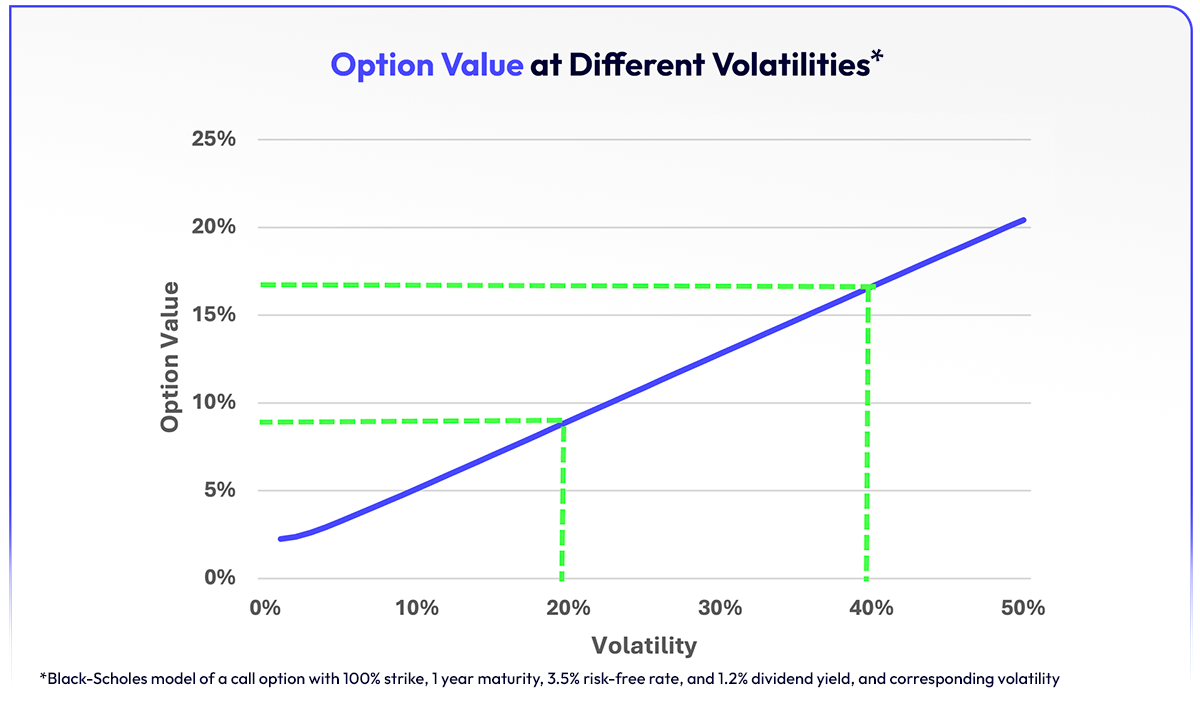

A call option grants the right to buy a stock at a fixed price before a certain date. If the stock barely moves, that right has little value. If the stock could surge significantly, the option can become very valuable. The downside on an option is capped at the purchase price, while the upside is openended, so more expected movement means more potential value. That is why higher volatility translates directly into higher option prices.

What "Implied" Volatility Means

Volatility is not directly observable in the market. Traders derive it from option prices using pricing models like Black-Scholes, which take a set of known inputs (stock price, strike price, time remaining, interest rates, dividends) and standardized assumptions and solve for fair value. Reverse the equation with a live option price, and the unknown becomes volatility.

That is implied volatility: the market's real-time estimate of how much a stock might move, embedded in every option price.

Every Stock Has a Different Implied Volatility

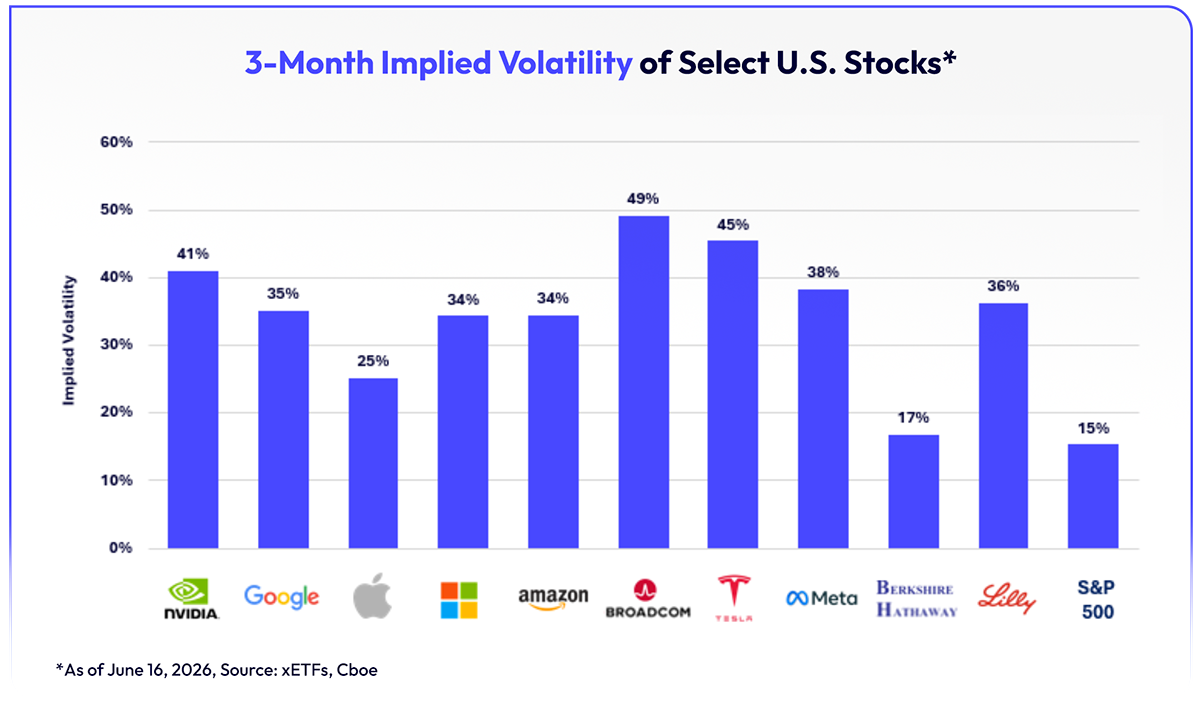

Not all stocks have the same levels of uncertainty, and the market prices those differences into options. Nvidia and Tesla carry higher implied volatility because neither is easy to forecast: Nvidia's trajectory depends heavily on AI demand, and Tesla's on the pace of autonomous vehicle adoption. Companies like Apple and Berkshire Hathaway, with more predictable revenue and diversified operations, have relatively lower implied volatility. The S&P 500 index sits lower still, since diversification reduces individual stock risk. Higher implied volatility means higher option premiums, across every name and every strike.

The Income Angle

Selling call options against stock already held generates income upfront, in exchange for agreeing to sell shares at a fixed price if the stock rises past that level. Higher implied volatility means higher premiums collected, which is why Tesla and Nvidia generate significantly more income from this approach than a utility company would.

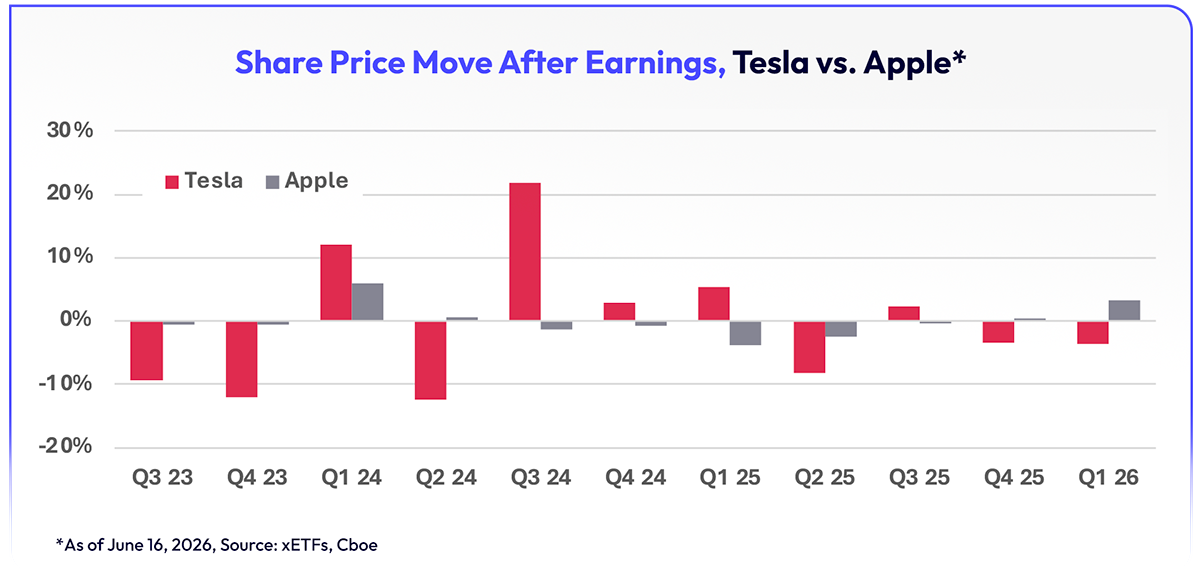

The tradeoff is real: if the stock surges past the strike price, that upside is forfeited. The same volatility that generates more premium also means the underlying stock can move more sharply in either direction. On average, Tesla moved 8.5% the day after its 10 most recent earnings releases, compared to 1.8% for Apple.

The Bottom Line

Implied volatility is the market's real-time expectation of future price movement, derived from live option prices. Higher implied volatility means higher option premiums, which means more income for sellers and more cost for buyers. It also explains why the same strategy may produce meaningfully different results across different stocks, and why the choice of underlying stock matters as much as the strategy itself.

This content is intended for educational purposes only. It does not constitute investment advice or an offer or solicitation and should not be used as the basis for any investment decision.

Carefully consider the Funds’ investment objectives, risk factors, charges and expenses before investing. This and additional information can be found in the Funds’ Prospectus and Summary Prospectus, which may be obtained by visiting www.xETFs.com/investor-materials. Read the Prospectus and Summary Prospectus carefully before investing.

Exchange Traded Concepts, LLC serves as the investment adviser. WallStreetX ETFs, Inc. dba xETFs serves as the sub-adviser. The Funds are distributed by Foreside Fund Services, LLC., which is not affiliated with xETFs, Exchange Traded Concepts, LLC, or any of its affiliates.

Investing involves risk, including possible loss of principal. The Fund’s return may not match or achieve a high degree of correlation with the return of the Index. To the extent the Fund’s investments are concentrated in or have significant exposure to a particular issuer, industry or group of industries, or asset class, the Fund may be more vulnerable to adverse events affecting such issuer, industry or group of industries, or asset class than if the Fund’s investments were more broadly diversified. Issuer-specific events, including changes in the financial condition of an issuer, can have a negative impact on the value of the Fund.

A new or smaller fund is subject to the risk that its performance may not represent how the fund is expected to or may perform in the long term. In addition, new funds have limited operating histories for investors to evaluate and new and smaller funds may not attract sufficient assets to achieve investment and trading efficiencies.

Shares are bought and sold at market price (closing price) not net asset value (NAV) and are not individually redeemed from the Fund. Market price returns are based on the midpoint of the bid/ask spread at 4:00pm Eastern Time (when NAV is normally determined) and do not represent the return you would receive if you traded at other times. Brokerage commissions will reduce returns.